Introduction

For anyone considering buying a home, understanding the concept of mortgage pre-approval is a crucial step in the homebuying journey. But what does it mean, why does it matter, and how can it benefit you? In this article, we’ll demystify the process of mortgage pre-approval and explore its significance in the world of real estate.

Mortgage pre-approval is a pivotal concept that every prospective homebuyer should grasp thoroughly. It serves as the foundational step in the homebuying journey, providing invaluable insights into your financial readiness, and it carries significant implications for your entire real estate experience. In this article, we embark on a journey to demystify the process of mortgage pre-approval, shedding light on its meaning, importance, and the multitude of benefits it offers to individuals seeking to make one of life’s most significant investments.

Mortgage Pre-Approval Defined:

At its core, mortgage pre-approval is a rigorous evaluation conducted by a lender to assess your financial health and determine your eligibility for a home loan. This process involves a comprehensive review of

If you’d like to dive deeper into this subject, there’s more to discover on this page: What Is a Mortgage? Types, How They Work, and Examples

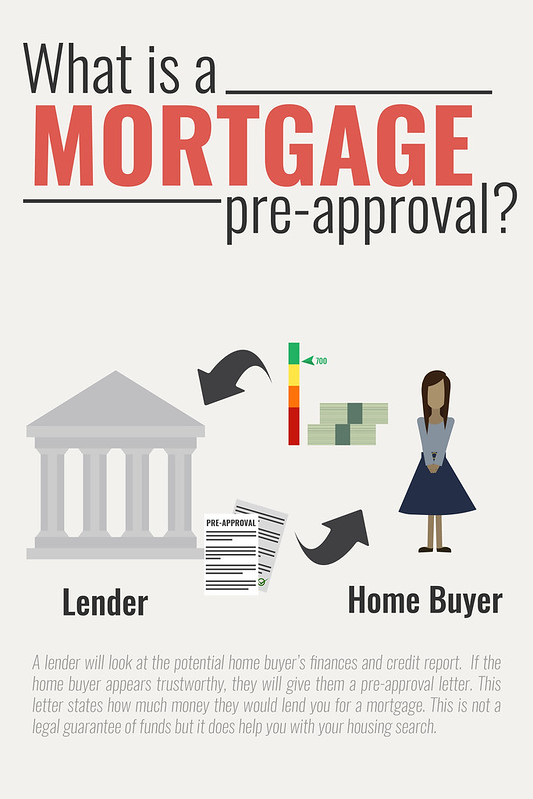

Mortgage pre-approval is a preliminary evaluation conducted by a lender to determine if you qualify for a home loan and, if so, how much you can borrow. Unlike pre-qualification, which is a more informal assessment, pre-approval involves a comprehensive review of your financial background, credit history, and employment status. It is a significant step towards securing a mortgage and becoming a serious contender in the real estate market.

Mortgage pre-approval is not only a crucial step in the homebuying process but also a strategic advantage. Here’s why it matters:

Streamlined Home Search: With pre-approval in hand, you have a clear understanding of your budget. This narrows down your home search to properties that you can comfortably afford, saving you time and effort.

Competitive Edge: In a competitive real estate market, sellers often favor buyers with pre-approval because it signifies that you’re financially ready to make an offer. This can give you an edge over other potential buyers.

Negotiating Power: Pre-approval provides you with negotiating power. When you submit an offer, sellers are more likely to take it seriously, knowing that your financing is in order.

Faster Closing: Since much of the paperwork and verification processes are already completed during pre-approval, the time it takes to close the deal can be significantly reduced. This can be particularly advantageous in a hot housing market.

Peace of Mind: Knowing that you’ve been pre-approved for a mortgage offers peace of mind during the homebuying process. You can confidently make an offer when you find the right property, knowing that financing is less likely to be a hurdle.

Clear Financial Picture: Mortgage pre-approval also gives you a clear financial picture. It highlights any potential issues that might affect your ability to secure a loan, allowing you to address them proactively.

In summary, mortgage pre-approval is more than just a formality; it’s a valuable tool that enhances your homebuying experience, increases your competitiveness, and simplifies the process of acquiring your dream home.

For a comprehensive look at this subject, we invite you to read more on this dedicated page: Mortgage Pre-Qualification vs. Pre-Approval – Understanding the …

You start by submitting a mortgage application to a lender or a mortgage broker. This application includes detailed information about your finances, such as income, assets, debts, and employment history.

“Your mortgage application is the crucial first step towards securing a home loan. It provides lenders with a comprehensive view of your financial situation, allowing them to assess your eligibility and determine the terms of your loan.”

Don’t stop here; you can continue your exploration by following this link for more details: Get a prequalification or preapproval letter | Consumer Financial …

The lender reviews your credit report and credit score to assess your creditworthiness. A good credit score is typically a crucial factor in obtaining pre-approval and favorable mortgage terms.

The process of obtaining pre-approval for a mortgage is a critical step in the homebuying journey, and your credit score plays a central role in this evaluation. Here’s a more detailed exploration of why a good credit score is essential for securing pre-approval and favorable mortgage terms:

Creditworthiness Assessment: When you apply for a mortgage pre-approval, the lender conducts a comprehensive assessment of your creditworthiness. This assessment involves reviewing your credit report, which contains a detailed record of your credit history, including past loans, credit card accounts, and payment history.

Credit Score Significance: One of the key factors lenders consider during this assessment is your credit score. This three-digit number, typically ranging from 300 to 850, provides a concise summary of your creditworthiness. A higher credit score indicates a lower credit risk, while a lower score suggests higher risk.

Risk Mitigation: Lenders use your credit score as a tool to assess the level of risk associated with lending you money. A good credit score signals responsible financial behavior, such as making on-time payments, managing credit accounts wisely, and maintaining a healthy credit utilization ratio. This reduces the lender’s perception of risk, making them more inclined to offer favorable terms.

Pre-Approval Eligibility: With a good credit score, you are more likely to meet the lender’s eligibility criteria for pre-approval. Lenders typically set minimum credit score requirements, and having a score above this threshold demonstrates your creditworthiness and ability to manage debt responsibly.

Interest Rates: A higher credit score not only increases your chances of pre-approval but also directly impacts the interest rate you are offered. Lenders often provide lower interest rates to borrowers with excellent credit scores. This means that a good credit score can lead to significant savings over the life of your mortgage, reducing your overall borrowing costs.

Loan Terms: In addition to interest rates, a strong credit score may also influence other loan terms, such as the size of your down payment requirement and the duration of your mortgage. With a good credit score, you may have more flexibility and negotiation power when discussing the terms of your mortgage.

Access to Loan Programs: Certain mortgage loan programs, such as those offered by government agencies like the FHA or VA, may have specific credit score requirements. A good credit score ensures you have access to a broader range of loan options and can explore programs that align with your financial goals.

Peace of Mind: Finally, a good credit score provides peace of mind throughout the homebuying process. It not only increases your chances of obtaining pre-approval but also instills confidence that you are in a strong position to secure favorable mortgage terms. This confidence can reduce stress and uncertainty during the homebuying journey.

In conclusion, a good credit score is a foundational element when seeking mortgage pre-approval and favorable loan terms. It reflects your creditworthiness, reduces the lender’s perception of risk, and opens doors to more financing options. Nurturing and maintaining a strong credit score is a proactive step that can significantly enhance your ability to achieve your homeownership goals.

Additionally, you can find further information on this topic by visiting this page: Pre-Qualified vs. Pre-Approved: What’s the Difference?

You’ll be required to provide various financial documents, such as tax returns, pay stubs, bank statements, and proof of assets. This documentation helps the lender verify your financial stability.

Furthermore, the lender will assess your debt-to-income ratio (DTI) to determine your ability to manage additional debt. A lower DTI, which indicates a healthier balance between your income and debts, can improve your mortgage eligibility and the terms offered. It’s essential to prepare your financial documents and work on reducing your DTI before applying for a mortgage to increase your chances of approval and secure favorable loan terms.

You can also read more about this here: How To Get A Mortgage Preapproval | Rocket Mortgage

Lenders assess your income to determine your ability to make mortgage payments. They may contact your employer to verify your employment status and income.

” Lenders assess your income to determine your ability to make mortgage payments. They may contact your employer to verify your employment status and income. It’s important to maintain stable employment during the mortgage application process.”

Additionally, you can find further information on this topic by visiting this page: Mortgage Preapproval: Everything You Need to Know | LendingTree

After a thorough review of your financial information, the lender decides whether to grant you pre-approval and, if so, the amount you’re pre-approved for.

“The process of obtaining mortgage pre-approval is akin to a financial health check-up, and it plays a pivotal role in your homebuying journey. Here’s a deeper dive into the significance and mechanics of mortgage pre-approval:

Financial Assessment: Mortgage pre-approval isn’t merely a formality; it’s a comprehensive evaluation of your financial standing. Lenders delve into your income, credit history, employment stability, debts, and assets. This in-depth analysis helps them understand your financial capacity to take on a mortgage.

Risk Assessment: Pre-approval also involves a risk assessment from the lender’s perspective. They aim to determine the likelihood of you repaying the loan based on your financial track record and current circumstances. This risk evaluation informs their decision regarding your pre-approval status.

Loan Amount Determination: Upon successful evaluation, the lender not only approves your mortgage application but also specifies the amount you’re pre-approved for. This figure represents the maximum loan amount the lender is willing to extend to you, based on their assessment of your financial capacity.

Confidence in House-Hunting: Armed with a mortgage pre-approval, you gain a significant advantage when house-hunting. Sellers and real estate agents take pre-approved buyers more seriously because they have already secured financing up to a certain amount. This can be a decisive factor in competitive real estate markets.

Budget Clarity: Pre-approval offers clarity regarding your budget. You know precisely the maximum loan amount you can access, which helps you focus your home search on properties within your financial reach. It prevents wasting time and effort on homes that are either too expensive or too far below your budget.

Negotiation Power: Having a pre-approval letter can give you leverage during negotiations. Sellers often favor buyers with pre-approval because it indicates a higher likelihood of a successful transaction. This can lead to more favorable terms and conditions when making an offer.

Streamlined Process: Pre-approval streamlines the mortgage application process once you find your ideal home. Much of the legwork, including the initial credit assessment and documentation verification, is already complete. This expedites the final loan approval process and moves you closer to homeownership.

Interest Rate Lock: Some lenders may allow you to lock in an interest rate at the time of pre-approval. This is particularly advantageous if interest rates are expected to rise, as it secures a favorable rate for your future mortgage.

Continued Financial Responsibility: It’s essential to maintain financial responsibility after pre-approval. Avoid taking on new debt, missing bill payments, or making major financial changes, as these can impact your final loan approval. Your financial stability should align with the information presented during pre-approval.

Limited Duration: Keep in mind that mortgage pre-approval typically has a limited duration, often ranging from 60 to 90 days. If you don’t find a suitable home within this timeframe, you may need to undergo the pre-approval process again, as financial circumstances can change.

In conclusion, mortgage pre-approval is a comprehensive financial evaluation that provides you with a clear budget, negotiation power, and confidence in your homebuying journey. It’s a valuable step that not only opens doors to homeownership but also sets the stage for a more efficient and informed real estate experience.”

For a comprehensive look at this subject, we invite you to read more on this dedicated page: Pre-Qualified vs. Pre-Approved: What’s the Difference?

Pre-approval gives you a clear understanding of how much you can afford to spend on a home. This knowledge helps you narrow down your search to properties within your budget.

“Pre-approval is your key to unlocking the housing market. By obtaining pre-approval for a mortgage, you gain a competitive edge when making offers on homes. Sellers are more likely to consider your offer seriously, knowing you have the financial backing to make the purchase. It also speeds up the closing process, getting you into your new home faster. So, don’t skip this important step in your homebuying journey.”

You can also read more about this here: 5 Things You Need to Be Pre-Approved for a Mortgage

In a competitive real estate market, having a pre-approval letter demonstrates your seriousness as a buyer. Sellers are more likely to consider offers from pre-approved buyers over those without pre-approval.

“Pre-approval is your ticket to a competitive edge in the housing market. It shows sellers you’re a serious and well-qualified buyer, potentially giving your offer an advantage over others. Getting pre-approved is a crucial step in your homebuying journey.”

To expand your knowledge on this subject, make sure to read on at this location: Mortgage Pre-Qualification vs. Pre-Approval – Understanding the …

Pre-approval can enhance your negotiating power when making an offer. Sellers may be more inclined to negotiate terms with a pre-approved buyer.

“Obtaining a mortgage pre-approval is a strategic move that can significantly bolster your position in the real estate market, particularly when it comes to negotiations with sellers. Here’s a deeper exploration of why pre-approval is a game-changer and how it enhances your negotiating power:

Credibility and Confidence: When you present a pre-approval letter to a seller, you’re demonstrating your seriousness and financial readiness to purchase their property. This level of commitment instills confidence in the seller, assuring them that you’re a genuine, qualified buyer.

Faster Transactions: Sellers often prefer buyers with pre-approvals because it expedites the closing process. Pre-approval indicates that your financing is well underway, potentially reducing the time it takes to complete the transaction. This can be especially appealing to sellers who are eager to move forward swiftly.

Price Negotiation: Sellers may be more inclined to negotiate on the sale price, terms, or concessions when dealing with pre-approved buyers. Your pre-approval reassures them that securing financing is less likely to become a hurdle in the negotiation process, making them more open to accommodating your preferences.

Competitive Advantage: In competitive real estate markets, where multiple buyers may be interested in the same property, having a pre-approval can be a game-changer. It sets you apart from other potential buyers who may not have taken this crucial step. Sellers are more likely to favor offers from pre-approved buyers in such scenarios.

Clarity on Affordability: A pre-approval clarifies your budget and what you can comfortably afford. This information is valuable not only to you but also to the seller. It ensures that negotiations are grounded in realistic expectations, reducing the likelihood of surprises or misunderstandings later in the process.

Flexibility in Contingencies: Pre-approval can give you greater flexibility when structuring contingencies in your offer. For example, you may have the confidence to waive certain contingencies or adjust timelines, making your offer more appealing to the seller.

Negotiating Leverage: When you’re pre-approved, you have the advantage of negotiating from a position of strength. This can be especially beneficial in situations where you’re seeking concessions or repairs following a home inspection. Sellers are often more willing to accommodate pre-approved buyers to keep the deal moving forward.

Reduced Risk of Deal Breakdown: Pre-approval minimizes the risk of the deal falling through due to financing issues. Sellers are generally more at ease knowing that you’ve already cleared a significant hurdle in the homebuying process.

In summary, obtaining a mortgage pre-approval is a strategic move that not only streamlines your homebuying journey but also significantly enhances your negotiating power. It fosters trust and confidence with sellers, potentially leading to more favorable negotiations on price and terms. A pre-approval is not just a piece of paper; it’s a valuable tool that can make your offer stand out and increase your chances of securing the home you desire.”

For a comprehensive look at this subject, we invite you to read more on this dedicated page: Buyer’s Guide: How To Negotiate House Price | Rocket Mortgage

Since much of the mortgage underwriting work is already completed during pre-approval, the closing process may be expedited, helping you move into your new home more quickly.

“Streamlined Closing Process: Pre-Approval Paves the Way for a Faster Move-In. Get Your Mortgage Approved and Home Sweet Home Sooner.”

For a comprehensive look at this subject, we invite you to read more on this dedicated page: Pre-Approval Process Explained by KFS Mortgage

Without pre-approval, you risk falling in love with a home that is beyond your financial reach. Pre-approval ensures that you shop for homes that align with your budget.

Additionally, pre-approval can make your offer more attractive to sellers in a competitive market, as it shows that you are a serious and financially qualified buyer. This can give you an edge when negotiating the purchase of your dream home.

For a comprehensive look at this subject, we invite you to read more on this dedicated page: Mortgage Pre-Approval Process in Washington State: The Benefits

Knowing you’re pre-approved provides peace of mind and boosts your confidence as you navigate the homebuying process.

The confidence that comes with mortgage pre-approval is a game-changer in the homebuying process. Here’s how it makes a significant difference:

Peace of Mind: Pre-approval assures you that a lender has already assessed your financial situation and is willing to lend you a certain amount for a mortgage. This peace of mind eliminates uncertainties about whether you can secure financing for your dream home. You can confidently focus on finding the right property without the nagging worry of whether you’ll be approved for a loan.

Competitive Advantage: In a competitive real estate market, where multiple buyers may be interested in the same property, having a pre-approval letter gives you a substantial advantage. Sellers view pre-approved buyers as serious and reliable. Your offer is more likely to be taken seriously, potentially putting you at the forefront of the negotiation process.

Focused Home Search: Knowing your budget through pre-approval streamlines your home search. You won’t waste time and effort on homes that are beyond your financial reach. This focused approach enables you to target properties that align with your budget, preferences, and needs, increasing the efficiency of your search.

Confident Decision-Making: With a pre-approval in hand, you can make informed decisions swiftly. You’re aware of your purchasing power and can confidently make offers when you find the right property. This decisiveness can be crucial in a competitive market where time is of the essence.

Financial Planning: Pre-approval encourages responsible financial planning. You’ll have a clear understanding of your future mortgage payments and can budget for other homeownership expenses accordingly. This proactive approach sets you up for successful homeownership with minimal financial stress.

Negotiation Leverage: Pre-approval provides negotiation leverage. Sellers are more inclined to work with pre-approved buyers because they know the financing aspect is secure. This can potentially lead to more favorable terms, such as price adjustments or contingencies.

Realistic Expectations: It helps set realistic expectations. You’ll know what you can afford, which prevents you from falling in love with homes that are outside your budget. This prevents heartache and ensures you remain focused on homes that align with your financial capabilities.

Efficient Closing Process: The mortgage pre-approval process typically involves a thorough review of your financial documents. As a result, the mortgage approval process after you find your dream home tends to be more efficient, potentially leading to a faster closing.

In essence, mortgage pre-approval is your ticket to a more confident, focused, and efficient homebuying journey. It not only provides peace of mind but also positions you as a serious and attractive buyer in the eyes of sellers and real estate professionals. With pre-approval in hand, you can navigate the complexities of the real estate market with confidence, making well-informed decisions and ultimately securing the home that aligns perfectly with your dreams and financial goals.

Additionally, you can find further information on this topic by visiting this page: A Crucial First Step: Mortgage Pre-Approval [INFOGRAPHIC …

Mortgage pre-approval typically has a shelf life of 60 to 90 days. After this period, lenders may request updated financial information to ensure your circumstances have not significantly changed. If interest rates rise during this time, you’ll still be eligible for the rate that was in effect at the time of your pre-approval.

Mortgage pre-approval’s shelf life is an important factor to consider in your homebuying timeline. Here’s why it matters and how you can navigate it:

Timing is Key: The 60 to 90-day window for mortgage pre-approval reflects the dynamic nature of the real estate and financial markets. By setting an expiration date, lenders ensure that your financial information remains current and that you’re still in a position to meet the loan requirements.

Interest Rate Protection: One significant advantage of pre-approval is that it locks in the interest rate at the time of your application. This means that if interest rates rise during the pre-approval period, your rate remains unchanged. It provides a safeguard against market fluctuations, potentially saving you money over the life of your mortgage.

Home Search Timing: Given the limited duration of pre-approval, it’s important to time your home search effectively. Start looking for homes within the pre-approval period to make the most of the locked-in interest rate and the advantage it offers in negotiations.

Financial Updates: If your pre-approval expires, don’t worry; it’s a common occurrence. Lenders may request updated financial information, such as bank statements, pay stubs, and credit reports, to re-evaluate your eligibility. As long as your financial situation hasn’t undergone significant negative changes, you should be able to renew your pre-approval.

Interest Rate Watch: Keep an eye on interest rate trends. If rates are on an upward trajectory and your pre-approval is about to expire, consider renewing it sooner rather than later to lock in a favorable rate.

Consult Your Lender: Communication with your lender is crucial throughout this process. They can provide guidance on when to renew your pre-approval and offer insights into prevailing interest rate trends.

In conclusion, while mortgage pre-approval does have an expiration date, it’s a manageable aspect of the homebuying process. By staying informed about interest rates, staying in touch with your lender, and planning your home search effectively, you can make the most of your pre-approval and secure the best possible mortgage terms.

Additionally, you can find further information on this topic by visiting this page: How Long Does A Mortgage Preapproval Last? | Rocket Mortgage

Conclusion

In conclusion, mortgage pre-approval is a critical step in the homebuying process. It empowers you with a clear budget, competitive advantage, and the confidence to make informed decisions. If you’re serious about buying a home, consider seeking pre-approval early in your journey to homeownership. It’s a valuable tool that can help you secure the home of your dreams.

“Summing up, mortgage pre-approval isn’t just a helpful step; it’s essential when buying a home. It equips you with a solid budget, a competitive edge, and the assurance needed to navigate the homebuying process confidently. If homeownership is your goal, don’t hesitate to pursue pre-approval early—it’s a crucial tool on your path to securing your dream home.”

Additionally, you can find further information on this topic by visiting this page: Loan terminology glossary | UCOP

More links

Looking for more insights? You’ll find them right here in our extended coverage: 5 Things You Need to Be Pre-Approved for a Mortgage